When we first meet with individuals and families about their finances, we typically sense apprehension and nervousness. Many times people have met with financial planners who have sounded like used car salesmen trying to recommend insurance policies right away.

In some cases, people are looking to replace financial advisors who just haven’t performed well or who are unresponsive and uncommunicative. And in all cases, opening up your personal books to a stranger can be inherently nerve-racking.

While the first meeting is an important one, we take a different approach and try to offer some educational insights that resonate with the high majority of people we work with daily. This information helps us understand the specific situation that the particular person or family is in, and more importantly it helps them determine right away if they’re on the right financial path.

Huge disclaimer: There is no “right” financial path that guarantees wealth and happiness. However, based on our experiences and understand of what works and what doesn’t when it comes to financial plans, we have developed what we believe to be a path that can help people accomplish their financial goals.

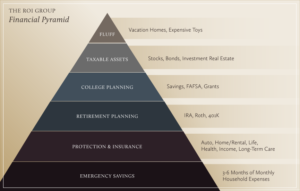

The ROI Group Financial Pyramid

We’ve taken the elements of what we believe to be a sound financial path and created a pyramid – more specifically, The ROI Group Financial Pyramid. We use this pyramid with every client, and typically present this chart both on first meetings with individuals and their families and many times after that as their financial plans, based on their goals, change during the course of their lives.

There’s a reason we decided to make a pyramid, and this is because its shape visually depicts both the importance and the order of where we feel people’s money should go. You’ll see this pyramid on all of our age group-focused pages as well as our services page for individuals and families.

Below is a breakdown of the different levels of the pyramid.

Level 1: Emergency Savings

Crucial to building your financial foundation.

As early as possible, and no matter what age you’re at, we suggest saving 3-6 months worth of household expenses. This includes rent/mortgage, utility bills, groceries, and anything else you make fixed to semi-fixed payments for each month.

Obviously, spending versus saving is a Superman versus kryptonite-type battle. Some people want to buy a boat or a fancy car, others want to pay off debt with low interest rates (like college loans) quickly just because it makes them feel better, and others want to play the stock market to keep up with their friends.

But without a nest egg of savings, not only will you not be able to afford a fancy car, you won’t be able to pay your rent or mortgage if you lose your job, get injured, or have a family emergency that keeps you out of work.

It’s not fun to think about sad and negative situations, and nobody thinks that anything bad will happen to them, but developing an Emergency Savings fund is the vital first step in building a solid financial plan

Level 2: Protection & Insurance

Protecting your biggest assets is key.

Once you’ve saved your 3-6 months of emergency funds, the next step is protecting yourself and/or your family.

You probably have auto and health insurance, which protect your car and your body when both need maintenance. If you own a home, you have homeowner’s insurance that protects it, and if you rent you might even have renter’s insurance that protects any number of things you own.

But are you protecting your biggest assets – your income and your family? If you get hurt or become disabled in some way and can’t work, your income goes away. And if something catastrophic happens to you, and your income goes away, how will your family be supported?

Exploring basic – and many times very inexpensive – disability, life, and other insurance as means of protecting yourself and your loved ones is critical when building a financial foundation.

Level 3: Retirement Planning

The earlier you start, the more money you’ll accumulate for later in life.

After you’ve built up your savings and protected your assets, it’s time to start thinking about saving for a different stage in your life: retirement.

We understand that it’s very difficult to think about saving money for a time so far down the road – especially when there are so many cool things to spend money on now!

But the fact is that people are living longer these days, and relying on Social Security funds to carry you is just not realistic anymore. Unfortunately, many times when you see elderly people working as greeters in Wal-Mart, the reason is because they miscalculated their retirement savings and need an income to live.

And imagine living your life now on a fixed income – it probably doesn’t sound so great.

The good news is that the earlier you start, the more money you’ll have later in life, thanks to the beauty that is compounded interest. There are various vehicles to use for retirement planning, including ones that you’re probably aware of such as 401k plans and Roth Individual Retirement Account (IRA).

Level 4: College Planning

The struggle is real – if you’re not prepared.

If you’ve chosen to have kids, you’ve probably already started thinking about college. What you probably haven’t thought about is how to save and pay for your kid’s education.

You’ve probably noticed that college costs are scary these days. Our clients share your fear. It’s not uncommon for a 4-year institution to cost the upwards of $150,000-$200,000 to attend, even after aid, grants, and scholarships.

Yet despite this reality, we can’t tell you how many people don’t start saving for college until their child is in high school. This puts enormous amounts of pressure on parents – and unfortunately, on relationships within the household.

Just like with retirement savings, there are multiple vehicles to save for college, such as a 529 Plan. And also similarly, the earlier you start saving even a little bit of money, the more money you’ll have as your child nears college age.

Level 5: Taxable Assets

Opportunities for additional income – with added risk.

If you’ve managed to save money for college and retirement successfully, you’ve reached the level of the pyramid where you might be able to add additional income streams.

Solid planning in the earlier sections of your financial plan may allow you to make some riskier investments. Brokerage accounts comprised of stocks, bonds, mutual funds, and other financial vehicles are among the taxable assets you could explore.

Buying additional real estate including investment properties are also options if you have capital to use.

While stock-trading is sexy and makes for great conversation, we recommend strategic investments to enhance your portfolio – and only recommend looking at these investments after the other pieces of the pyramid are solidly in place.

Level 6: Fluff

Your financial plan in action.

Unfortunately for most people, the “fluff” level of the pyramid is where all the fun happens. This is the time where you execute the bulk of your financial plan.

Your hard work in saving money pays off at this level. Ideally, your income streams come from not just Social Security but also from retirement savings accounts, insurance policies, and potentially sound investments.

Travel and exotic vacations, vehicles, toys, and other big purchases are more easily justifiable and finally fundable.

NOTE: These are the opinions of the author and not necessarily those of Cambridge; they are for informational purposes only, and should not be construed or acted upon as individualized investment advice.

No Comments